Shares of Arcam AB, NASDAQ OMX (ARCM.ST) and American Depository Receipt (AMAVF), have dropped 52% from January highs. Investors in 3D printing stocks are now (fortunately) taking fundamentals into consideration and the companies with the strongest growth in 2014 will rightfully be the best performers going forward.

I believe Arcam shares are now undervalued and have begun to re-enter my position based on the following:

- Arcam’s 70% organic revenue growth in Q1 with a strong outlook for continuation of the same

- Strategic acquisition in February of a high-grade titanium powder supplier expected to increase sales of both materials and ultimately, machines

- December’s launch of the Arcam Q-20 for aerospace market

- European Union-funded R&D from which Arcam is the patent assignee and ultimate beneficiary

Arcam & EBM Technology Overview

Based in Sweden, Arcam is the developer of the patented EBM (Electron Beam Melting) technology, which produces metal components that are more dense than 3D printed parts using Direct Metal Laser Sintering (DMLS). Arcam’s EBM printers are primarily used in the aerospace, defense, and orthopaedic implant markets.

In its report “3D printing: A potential game changer for aerospace and defense” PricewaterhouseCoopers notes that: “EBM has emerged as a higher quality alternative to laser melting. The very high-energy density of the electron beam technology enables it to produce fully dense, void-free parts.”

PwC also states: “The biggest hurdle to mass adoption is processing speed. Because of its intricate, layer-by-layer nature, current 3D printing technology takes hours to days to complete jobs. This cycle time is sufficient for prototypes and very small production quantities, but it quickly becomes untenable at higher production volumes. However, advances in electron beam and powder feedstock technologies may enable higher speeds, making EBM a viable production technology suitable for many more applications, including those for most aerospace and defense programs.”

Following a 4:1 share split in January, Arcam has 18.3 million shares outstanding.

Higher Organic Revenue Growth Than 3D Systems and Stratasys

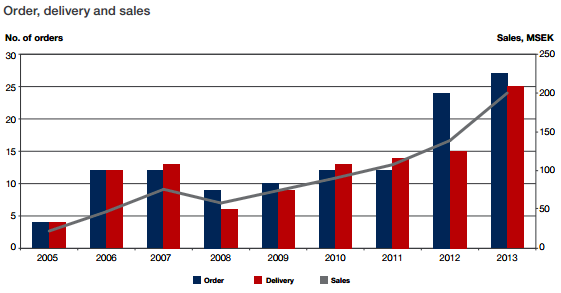

Arcam reported an impressive 43% organic sales growth in 2013, a much healthier rate than the 30-36% organic growth reported last year from both Stratasys (SSYS) and 3D Systems (DDD).

Q1 2014 Growth Accelerated to 70% Versus 45% at 3D Systems and 54% at Stratasys

In its Q1 release, Arcam’s sales growth (almost entirely organic) increased to an impressive 70%, a figure any other 3D printing OEM would love to have. Also recorded in Q1 was Arcam’s cash acquisition of high-grade titanium powder supplier Advanced Powders and Coatings. According to management’s Q1 conference call, this strategic acquisition is expected to increase machine sales going forward due to Arcam’s supply and control of the highest grade titanium powder on the market today. Arcam ended Q1 with a cash balance of 368 million SEK ($56 million USD) and no long-term debt.

By comparison, 3D Systems reported 45% revenue growth and Stratasys (last Friday) reported 54% revenue growth.

The forward-looking statements from the Q1 report were strong:

“In addition to the acquisition of AP&C we are in rapid organic growth. We thus continue to recruit qualified employees in order to meet the expectations from our customers. During the quarter we have strengthened our service office in China and the support organization in Sweden. Through the acquisition of AP&C and through recruitment the number of employees has increased from 55 to 109 since March 2013.”

And:

“An order book of 13 systems, increasing aftermarket sales and a positive business situation lays a solid foundation for a continued strong growth in 2014.”

Q2 Starting Strong

While sales (recorded at time of delivery) can be choppy, Arcam is off to a strong Q2 for their first half 2014 report scheduled for July 18th. In the first half of 2013 Arcam delivered 11 printers. In the first quarter of 2014 alone, Arcam delivered 7 printers with a backlog of 11 more printers. Since the Q1 report Arcam also announced orders from China, New Zealand, the United States, and a major manufacturer in the aerospace industry.

Canaccord Genuity stated in a January article that: “We believe Arcam’s revenue growth will be well above that of the 3D printing industry, driven by penetration of tier-one orthopaedic implant customers and a ramp to volume production by aerospace customers.”

Arcam Q20 Launch

Launched in December, the new Arcam Q20 is aimed squarely at the aerospace industry and features improved resolution, larger build envelope and inline part quality verification. Process speed has been greatly improved to the point of “manufacturing” capabilities, according to an article covering the Q20 launch in TCT Magazine.

Updating the Q20 launch in its Q1 conference call, management revealed that they have “several large customers positioning themselves for large volume production” from which Arcam expects to announce sales of multiple units per order this year.

In the Q1 press release, CEO Magnus Renee also stated:

“Arcam Q20 is planned for delivery to the first customers during the second quarter. The work to industrialize our technology with the major players within the aerospace and implant industries continue and we can now see good opportunities for volume orders during the year.”

As a result, I believe it’s a matter of time before Arcam announces as many as 3-5 or more printers in a single order.

Fast EBM Project Commercialization

“Fast EBM” is a completed 2-year project funded by governments of the European Union. The project’s goal is to increase printing speeds in high-grade metal components using enhanced EBM technology by a factor of 5X. Arcam led the project and is the recipient of all intellectual property and commercialization rights.

The recent project update on the Cordis website indicates:

-High productivity EBM machine: Designs have been produced and parts are being manufactured

– FastEBM pre-qualification for aerospace components manufacture: These tests will commence once the testbed equipment is established

– High power EB gun design: A 10kW gun design has been made and this is under manufacture

– Low-aberration deflector system: A number of deflection systems have been analysed and a design developed. Drive electronics have been considered and a design proposed. This is now being manufactured ready for test.

– Manufacturing process model: Software has been developed to enable beam powder interaction to be modelled.

Full-scale commercialization of this new high-speed EBM printer is expected next year.

TiAlCharger Project- Development of 3D Printed Titanium Aluminide Automotive Turbochargers

The TiAlCharger Project, (also funded by governments of the European Union), aims to create a cost-effective, mass producible, low inertia titanium aluminide (TiAL) turbocharger using Arcam’s EBM technology. Expected outcomes of the project are:

– Weight savings of 60%

– A reduction on mass moment of inertia of 36% (compared to Nickel super alloys that are the current state of the art)

– Operation at temperatures >950°C

– Increased fuel to air ratios thereby improving vehicle efficiency by an additional 5% and reducing CO2 emissions by 8%.

Arcam’s EBM process will fabricate a hollow, lightweight, low-inertia titanium aluminide rotor-wheel. The TiAl wheel turbine will be joined to the steel shaft using electron beam welding. This fabrication method provides the possibility to manufacture turbocharger wheels from TiAl, which (if of the required quality) retains its strength at high temperatures, expanding the usage of turbochargers to a broad range of engine types.

While potential commercialization from this project is farther off (project completion date is projected for 1/2015), Arcam should realize a healthy percentage of the “revenues worth an estimated 58 million euros” ($80 million US) from this new market.

Conclusion

3D printing stocks made a parabolic move last year that could not be sustained by their fundamentals. They’ve since given up that move and investors are focusing on revenue growth, particularly organic growth that’s free from integration costs and share dilution.

Based on Arcam’s higher growth rate than 3D Systems and Stratasys, their strong balance sheet, launch of the Arcam Q20, cash acquisition of Advanced Powders and Coatings, strong order book, strong forward-looking statements, and position in the high growth industrial metals segment, I believe shares are oversold and should soon see a move to the upside.

Disclosure: I am long shares of Arcam AB. I have not been paid by Arcam or any third-party for this article.