A new report from CONTEXT highlights mixed results for Q1 2023 across the 3D printing industry, with attention being drawn to mergers and acquisitions (M&A) amidst inflation and increasing demand for high-end systems. Companies are vying to establish the world’s first $1B+ 3D printing company, with growth in product shipments varying across sectors. Despite the fluctuation in unit shipment growth, system revenues have risen due to inflationary price increases and a shift in demand towards higher-end metal systems.

Three of the world’s largest 3D printing companies, Stratasys, 3D Systems, and Desktop Metal, have been in the spotlight, with Stratasys at the center of M&A activities. Stratasys was set to merge with Desktop Metal until more recent events this week called this course of action into question. CONTEXT states, “continued offers from 3D Systems, and from nascent player Nano Dimension, leave the industry guessing.

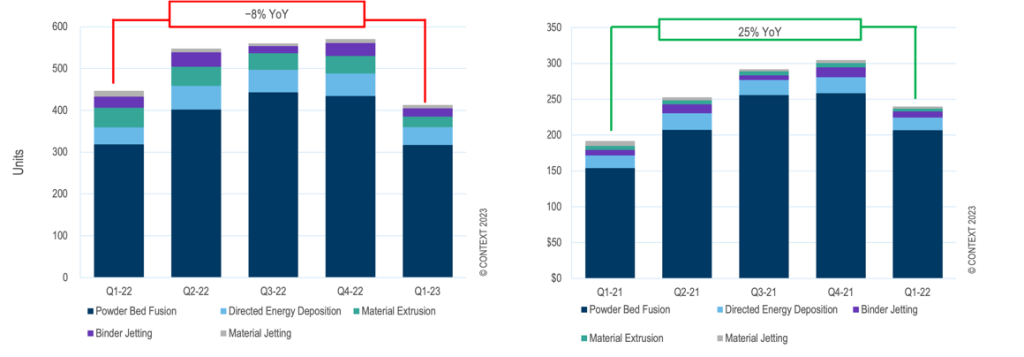

Global shipments of new additive manufacturing systems in the Industrial and Professional price classes have declined year-on-year (YoY) by −15% and −30% respectively in Q1 2023. However, the Midrange, Personal, and Kit & Hobby categories have seen a rise in shipments by 18%, 34%, and 29% YoY respectively. Despite the decline in some categories, revenues from system shipments have increased, leading to an overall total system revenue growth of 15% on the previous year.

The YoY fall in global shipments of Industrial 3D printers, which account for 54% of total system revenues, is primarily due to weaker sales of polymer systems. However, this did not affect revenues, which saw an 11% YoY rise driven by growing demand for higher-efficiency metal machines. The largest segment, vat photopolymerization, saw the sharpest drop in sales, with a decline of 33% across most geographies.

Industrial metal 3D printers have performed better, with revenues rising 25% YoY in Q1 2023 despite a decrease in unit sales by 8%. Powder bed fusion (PBF) printers accounted for 77% of metal system shipments, with revenues for Industrial PBF systems rising by 34%. This growth was driven by companies like Velo3D and SLM Solutions, which offer sought-after multi-laser, large build-volume machines.

The 18% YoY growth in unit shipments of Midrange 3D printers was driven by new products and strong domestic demand in China. Formlabs’ polymer PBF Fuse line and UnionTech’s vat photopolymer DLP offerings were significant contributors to this growth. However, shipments of Professional 3D printers dropped significantly in Q1 2023, down by 30% YoY, although revenues fell only by 15% YoY as the weighted pricing rose 21% to $7,271.

Despite excellent sales of lower-end, consumer-centric Personal and Kit & Hobby printers in Q1 2023, full-year growth expectations for the category remain subdued. This is attributed more to improved supply-chain logistics than to new demand. However, Bambu Lab has seen fantastic demand, allowing them to move from crowdfunding into mainstream commercialization, securing the number two global market share position in the quarter. Creality is ranked at number one.

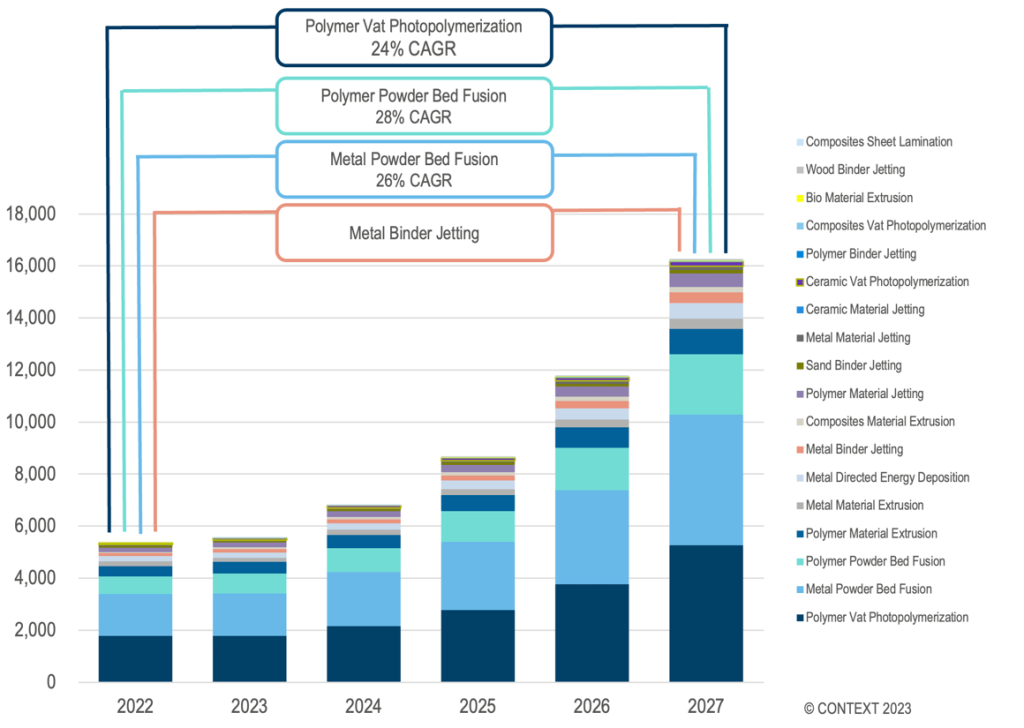

Looking ahead, while much of the industry’s attention has been on Western company consolidation, vendors like China’s Farsoon have continued the trend in the Asia–Pacific region of going public via traditional IPOs. The prospects for 3D printing remain bright, with demand growing and accelerating. The industry continues to excel in prototyping, with ample room for growth in mass customisation, low-volume production of complicated parts, and volume mass production. Technologies such as vat photopolymerization, PBF, and binder jetting are poised to meet these mass production needs, with metal PBF leading the Industrial market and on track to see a 5-year shipment CAGR of +26%.

What does the future of 3D printing for the next ten years hold?

What engineering challenges will need to be tackled in the additive manufacturing sector in the coming decade?

To stay up to date with the latest 3D printing news, don’t forget to subscribe to the 3D Printing Industry newsletter or follow us on Twitter, or like our page on Facebook.

While you’re here, why not subscribe to our Youtube channel? Featuring discussion, debriefs, video shorts, and webinar replays.

Are you looking for a job in the additive manufacturing industry? Visit 3D Printing Jobs for a selection of roles in the industry.

Featured image shows Industrial Unit Shipment Forecast by ASTM Process and Material via CONTEXT.